Interview #1: Japan Search Fund Accelerator

Interview #1: Japan Search Fund Accelerator

Japan's first & only search fund investment group is introducing a nuanced version of the entrepreneurial private equity concept into an SMB market in dire need of talented, young successors

Japan Business Insights (“JBI”): For our very first interview on Japan Business Insights, we have Hajime Shimazu-san (“HS”), the CIO of Japan Search Fund Accelerator (“JaSFA”). Welcome, Shimazu-san, and thank you for speaking with us today. We’re excited to have you shed some light on the nascent search fund industry in Japan today. To kick things off, could you please provide us with a brief overview of your professional background?

HS: Sure. Before jumping into things though, I want to thank you for the opportunity to share a bit about JaSFA. I believe the idea behind Japan Business Insights is both really exciting and very valuable as well.

With regards to my background, I spent 5 years with Boston Consulting Group (“BCG”) and a subsequent 6 years with Bain Capital in Tokyo, Japan. During my time with BCG, I was predominantly focused on supporting Japanese companies with their growth strategies, new business development & M&A, specifically in the TMT space. After BCG, I joined Bain Capital and was able to experience the entirety of the private equity investment process from deal sourcing through the ongoing support of portfolio companies. While at Bain, I was fortunate to earn my MBA at U.C. Berkeley as well.

JBI: Your background & skill set are rather fitting for the search fund space. Do you mind briefly explaining what exactly JaSFA is & how you came to be interested in search funds?

HS: So, JaSFA identifies, invests in & supports searchers in Japan. Since the Japanese search fund industry is still in its infancy today, there is an extremely limited pool of individual investors who are comfortable backing searchers, let alone those who even grasp the general concept of the search fund approach & model. To overcome this knowledge & funding gap, we formed JaSFA in 2018 and officially launched a fund of search funds in 2019 to specifically invest in a portfolio of high-quality, vetted searchers. In a way, you could say we proactively incubate search funds. Today, we now support six searchers, with one already having acquired a company.

As for how we came to focus on the search fund asset class, my wife, also an ex-BCG consultant, attended Stanford for her MBA and was fortunate to attend a lecture where she was introduced to the search fund concept. After spending a good bit of time learning more about the search fund industry, we quickly came to believe that the general model would fit very well within the Japanese market. At a high level, we feel that Japanese companies often have very strong operational execution, though are lacking when it comes to management’s strategic execution & capital allocation capabilities. Not only that, but given the seniority based promotion practices in Japan, the more ambitious, innovative minded younger generations are all but required to wait until their late careers to step into management positions in companies of almost any size. We are excited to leverage the search fund model to better connect small businesses (“SMEs”) - the backbone of the Japanese economy - with driven, entrepreneurial young talent capable of unlocking the significant latent potential of an increasingly challenged & vital segment of the Japanese economy.

JBI: That is very interesting. Let’s briefly address your last comment there a bit. Can you share some insights about the small business landscape in Japan today? Why is this market segment so challenged?

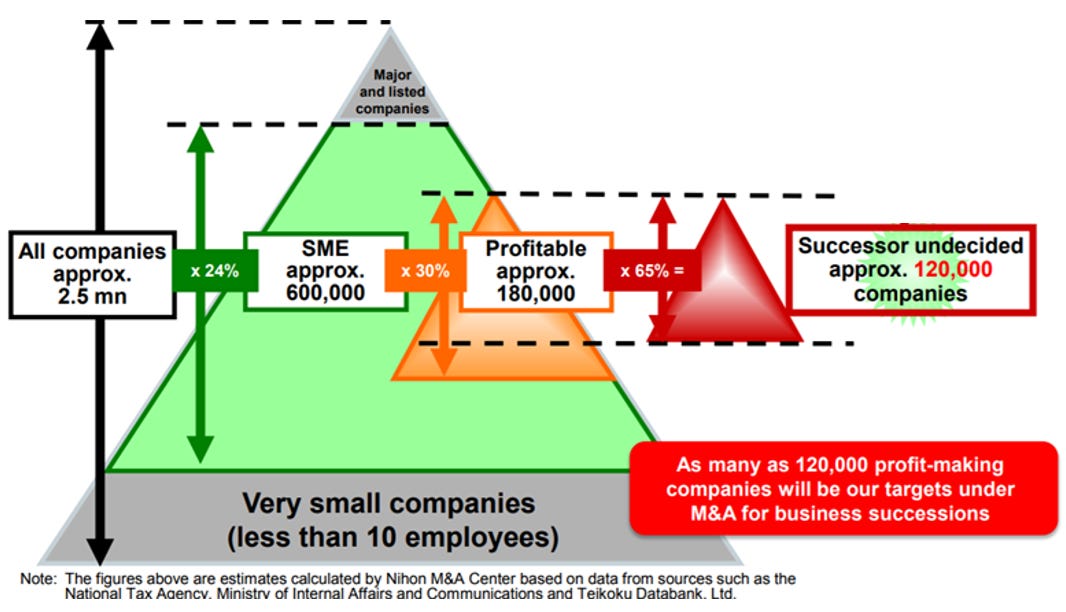

HS: I’ll try to remain brief, but of the 4.2M businesses in Japan, 4.19M, or 99%, are SMBs. SMBs employ >70% of the aggregate Japanese workforce and account for >60% of GDP. The median age of an SMB owner / CEO is 66 years old today, up from 47 years old 20 years ago. Notably, about 200k SMBs are shut down each year largely due to a lack of a successor. The more rural the company, of course, the more difficult it is to find a successor, with around 50% of SMBs having no viable direct successor (i.e. a family member). Historically, selling one’s business has also not been viewed very positively, however, this is slowly changing with several large SMB focused M&A advisory firms leading the charge in educating the SMB owner community about the merits & upsides in selling their businesses.

Japan SMB Market Size

Nihon M&A Company Presentation

JBI: That’s a great point. It has been fascinating to watch the likes of Nihon M&A Center, the leading SMB focused M&A advisor in Japan, aggressively grow both its operations and market capitalization over the last decade.

So, more specifically about search funds, how would you describe the state of the search fund industry in Japan today? How many active search funds exist in Japan at the moment?

HS: While it is tough to say exactly, we believe that JaSFA supports all of the existing search funds in Japan today - it is an industry truly in its infancy. From our understanding, there are currently just six active search funds in Japan. Five of them are directly backed by JaSFA (more on this below) & the sixth is in the form of a traditional search fund, as practiced in the U.S. (i.e. a number of individual investors invest in a single searcher who independently sources & closes a deal). JaSFA is an investor in this individual searcher as well. As it relates to challenges confronting the budding Japanese search fund industry, I would highlight the following factors:

Investors

There is a very limited pool of Japanese individual investors, and zero institutional investors, with the risk-appetite to back such a “new” type of investment opportunity. Most high net-worth individuals interested in “alternative investments” will often turn to tech angel investing. There is simply not enough awareness nor ongoing education about search funds in the domestic market yet - we hope to slowly change this.

The lack of a track record for the search fund asset class, particularly in Japan, is a significant hurdle. Without one, gaining trust in the model is difficult, particularly among institutional investors. We are excited by the fact that we are building not only our own personal investment track record, but also that of the entire search fund industry today.

While international investors may be more familiar with the search fund concept, many find it difficult to understand the Japanese market, which, of course, has a number of unique features that are distinct from other global markets, like the U.S.

Searchers

Historically, young talent is highly incentivized - particularly from a cultural / societal perspective - to seek employment within large companies. Life-time employment is the defacto reality when working for many of these established businesses. This is slowly changing, however. In our own searcher recruitment efforts, we have seen a clear uptick in the number of Japanese MBAs who are both aware of and interested in the search fund model. As more successful domestic search fund case studies emerge, we feel this growing excitement about the concept will accelerate.

SMBs

As mentioned earlier, many SMB owners feel a sense of shame in selling their company, though this is also slowly changing with time.

JBI: We have come to understand many of those same challenges in our own exploration of the SMB space in Japan. It is indeed a unique market.

Now, with regards to deal sourcing, how does that work in Japan?

HS: Quite simply, to gain access to deal flow, you need to establish & build relationships with local banks, SMB M&A advisory firms & local accounting or tax offices. Cold-outreach efforts are ineffective in Japan for cultural reasons.

JBI: Understanding the culture some, we can see how that is the case. So, let’s say you do find a potential deal, is it difficult to convince owners to ultimately sell?

HS: While difficult, it is not insurmountable by any means. Ensuring you properly frame the narrative around the purpose and realities of the search fund - so, downplaying the monetary upside potential & highlighting the ability to sustain the business & allow a young businessman to follow in the SMB owner’s footsteps - is essential.

JBI: What about deal financing? Is obtaining bank debt difficult?

HS: Interestingly, obtaining debt financing is much easier in Japan than I believe is the case in the U.S. A good relationship with a local bank is very helpful in this process, however.

JBI: I’ve personally heard mixed things about obtaining bank financing for SMB transactions in Japan, but perhaps sharing a bit more about your specific approach and model may help clarify things some?

HS: Sure. So, initially, we spent a lot of time studying the search fund industry in the U.S. We spoke with many potential investors and searchers during this process. At the time, we concluded that raising investment capital from U.S. investors would be too difficult. Back in Japan, we ended up speaking with about 50 individual & institutional investors in total. It was a time-consuming process, but we were fortunate enough to eventually secure a partnership with a local bank. Without question, finding an investor(s) has been the hardest part in building JaSFA so far - this was due to, again, the unproven nature of not only the search fund concept in Japan, but also our lack of a track record in executing our proposed search fund investment vehicle.

With regards to how exactly we are structured, I will break it down as follows:

Our bank partner is Yamaguchi Financial Group (“YMFG”). Our partnership with them looks like the below:

YMFG is the sole LP

YMFG & JaSFA are co-GPs

Searchers target companies in the three prefectures where YMFG has a presence, namely, Yamaguchi, Fukuoka, and Hiroshima prefectures

YMFG shares information with the searchers about their SMB clients & facilitates introductions to the SMB owners. This is critically important and a very valuable advantage in Japan

YMFG will provide any necessary debt financing to close the transaction, though existing debt is often rolled over as the SMB is already an existing client of YMFG

Within this framework, we currently back five active searchers, with one having already acquired a company

As mentioned earlier, JaSFA also backs a traditional independent searcher, Mr. Kurosawa, who manages JBS Partners. JaSFA invested alongside ~15 other individual investors from around the globe.

JBI: What a fascinating model - it would appear to significantly de-risk & accelerate the deal execution process given how closely you and the searcher work with your bank partner. We are not aware of any local banks partnering with searchers like this in the U.S.

Could you elaborate more on JaSFA’s core activities?

HS: So, JaSFA specifically focuses our efforts on two areas:

Recruiting Searchers

I would say 70% of our “searcher leads” are direct outreaches by those visiting our website or lectures, while the remaining 30% comes from personal relationships we actively seek to cultivate (e.x. Bain Capital, BCG, Tokyo University, international MBAs). We sometimes also organize general information sessions with large groups of soon-to-be and current MBAs to introduce the search fund model. Also worth mentioning, searchers receive ~40% of the acquired business at the moment, as the perceived risk is high for an unproven career path in Japan, coupled with the need to live & work in a limited geographic area outside of core population centers.

We also spend a significant amount of time trying to assess candidates before backing them. While prior relevant career experience and success is important, it is not all that we look for. We usually interview candidates for about three hours to evaluate their critical thinking and communication skills, while also trying to gauge how entrepreneurial they truly are. Previous work experience at name-brand companies is very helpful, particularly among SMB owners, while specific industry knowledge and previous management experience are nice-to-haves.

The three biggest obstacles in recruiting searchers are:

Our current lack of a track record - we have only closed a single transaction so far.

The strong negative stigma associated with “failing” in Japan. It is tough for potential searchers to come to terms with the prospect of perhaps failing to secure a transaction or properly managing the company as CEO once acquired.

As touched on earlier, working at a large company with a strong brand name infers a lot of social status in Japanese society and often comes with life-time employment guarantees. This is slowly changing, but is still a strong pull among young talent.

Value-Add Board Members

We are also active board members supporting searchers in due diligence, financial analysis, negotiations & post-acquisition value creation efforts.

JBI: Not an easy set of obstacles to overcome in terms of recruiting searchers. In the U.S., it is, at this point, much more of an active choice on the part of searchers, given how widely known the search fund concept is, particularly among MBAs.

Alright, so, let’s assume you have recruited a new searcher. What type of businesses are they typically looking to acquire? Also, what do typical acquisition multiples look like today for your targeted businesses?

HS: In general, we do not target a specific set of industry verticals. Our searchers are more opportunistic in nature, particularly in light of our relationship with YMFG. We do, of course, look for stable customer demand, above average local competitive dynamics, an overall simple business model and limited technology risk. Again, we have so far completed just one deal, but acquisition multiples generally fall within the 4x to 7x EBITDA range. Because of our close relationship with YMFG, most of our deals are proprietary, non-auctioned opportunities, where we focus more on the potential upside opportunity vs. the precise size metrics of a company. Generally speaking, though, we focus on businesses with $3M to $20M in revenue.

Also worth noting, inside the SMEs we typically target, “best practices” are usually lacking and the use of really any IT is almost always a rarity. Do realize that compensation levels within SMEs are often low & entirely based on seniority, however, Japanese workers tend to be very diligent and hard-working. So, human labor is usually deemed good enough versus feeling the need to pursue the unknowns involved in attempting to improve efficiencies via technology or unfamiliar business practices. Post-acquisition, we work closely with our searchers to really improve just about every aspect of the business. This is easier said than done, of course, given the entrenched employee expectations & processes & so on.

JBI: It sounds like there is significant upside in optimizing the business once acquired. After doing so, how does JaSFA plan to exit its investments?

HS: In most cases, we’ll likely look to exit individual investments via a sale to a regional strategic. An IPO is certainly viable given the reality that very small companies can IPO in Japan, however, we would likely want to first acquire at least several “bolt-ons”, which will take time and perhaps additional outside investment. The remaining alternative we’ll naturally consider is a management buyout should the searcher choose to remain as the CEO beyond the initial three to seven year investment period.

JBI: How do you see JaSFA growing & evolving over the next decade?

HS: Quite simply, our aim is to establish a new, larger fund that covers the entirety of Japan. The exact timeline depends on our ability to establish an initial track record and to further grow the awareness of JaSFA among searchers, bankers, investors and ultimately SMB owners. If I had to guess a rough “kick-off” date for this initiative, I would say within the next 18 months or so.

JBI: Very exciting! That is not too far off.

A very relevant question for our readers, how difficult is it for international investors to tap into the Japanese search fund space today?

HS: Good question. It is admittedly very difficult at the moment, as there are few independent searchers today in Japan, unlike in the U.S. Of course, our goal is to open up our Fund II to international investors, which we feel will be a compelling offering that will allow investors to gain exposure to an array of searchers with the added support of our likely growing team at JaSFA. To that end, I would encourage any international investors interested in learning more about the Japanese SMB market and future opportunities among Japanese search funds to reach out to us! You can check out our website and send us a note via our Contact Us page.

JBI: We would second that to any readers out there. Japan is a very unique, highly attractive and untapped market for the search fund model. There is far more to the opportunity than we have been able to cover here though, so please do reach out to Shimazu-san to dig a bit deeper.

Alright, to close things out, we plan to ask the following question to every interviewee. What is one thing about Japan that you really love?

HS: The food and the people! Food here in Japan is just so good and cheap. Tokyo is one of the global epicenters for delicious food. Japanese people are also very hard-working, diligent & quite friendly. From a business perspective, I would say the operational capabilities and standards of Japanese companies are some of the highest in the world. This fact is the primary driver of my own personal investment thesis on Japanese SMBs.

JBI: Hard not to agree with all of those points!

Well, we can’t thank you enough, Shimazu-san, for sharing your story and insights today. We’re excited to follow JaSFA’s success moving forward!

HS: Of course. Thank you for the opportunity!