tsukuruba: Building The Redfin - And Soon-To-Be Opendoor - of Japan

Overlooked & misunderstood by investors, tsukuruba is in the early stages of fully digitizing & redefining the end-to-end buying experience within the nascent & growing renovated home market in Japan

We’ll state from the outset that we presently view the opportunity with tsukuruba to be an “early-stage venture investment available in the public markets.” One could argue a good number of the more innovative, younger publicly listed technology companies in Japan today fall in a similar bucket given the relatively early IPOs most pursue, however, the case is particularly so for tsukururba, where significant market & execution risk remains.

Further supporting our above perspective is the fact that tsukuruba is today a “micro-cap” company, with a market capitalization of just ¥6.8Bn (~$65M), down from ~¥19Bn (~$180M) at its IPO in July 2019.

That being said, we believe the generally shorter term focused, less sophisticated retail investors who tend to dominate the tech-heavy small cap Mothers exchange simply do not understand and / or appreciate the longer-term vision of & ongoing progress being made by tsukuruba. Looking out five to ten years, we view the risk-adjusted, probability-weighted likelihood of tsukuruba being then valued at many multiples of its current valuation to be a highly attractive, asymmetric bet…one worth aggressively adding to as the thesis continues to hopefully play out over the ensuing years.

So, without further ado, let’s get into it!

Note: where none is attributed, the source is tsukuruba’s publicly available company materials.

tsukuruba was founded in August 2011 by Hiroki Murakami san & Masahiro Nakamura san with the initial aim of building a co-working business. Since then, the company has evolved to now encompass three distinct business units:

cowcamo - an end-to-end online real estate platform for the buying & selling of renovated, used residential properties. In short, a Japanese Redfin increasingly building towards a Japanese Opendoor.

Shared workplaces - which includes:

tsukuruba studios - a hyper-creative team tasked with incubating new design, architectural & related business concepts to infuse throughout the company

Similar to management, our focus is on tsukuruba’s fast-growing cowcamo offering, a business with the potential to entirely redefine & power Japan’s already shifting residential real estate market.

A Bit of Background: The Japanese Residential Real Estate Market

As a point of comparison, existing & new home sales accounted for 89% & 11% of total home sales, respectively, in the U.S. in 2019. On the opposite end of the spectrum, Japan has never historically had much of a home resale market, accounting for just ~15% of total nationwide home sales according to somewhat dated, though still roughly accurate Japanese government statistics (shared below).

Cultural proclivities play a role here, though there are other more fundamental reasons as well:

“Unlike in other countries, Japanese homes gradually depreciate over time, becoming completely valueless within 20 or 30 years. When someone moves out of a home or dies, the house, unlike the land it sits on, has no resale value and is typically demolished. This scrap-and-build approach is a quirk of the Japanese housing market that can be explained variously by low-quality construction to quickly meet demand after the second world war, repeated building code revisions to improve earthquake resilience and a cycle of poor maintenance due to the lack of any incentive to make homes marketable for resale.”

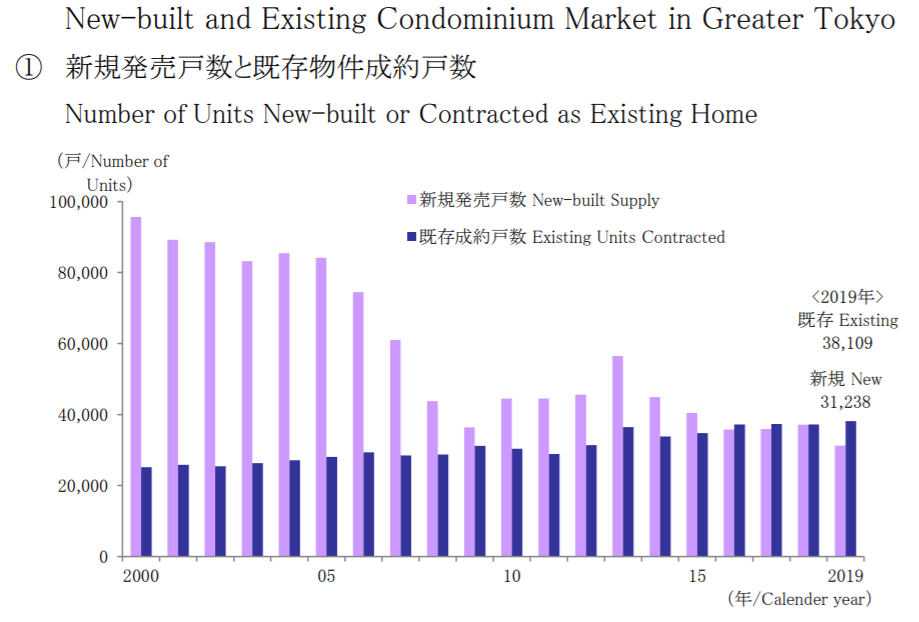

That notwithstanding, this reality is fast-changing. The below graphic from Mitsui Fudosan, a $17Bn market cap publicly listed real estate company in Japan, illustrates the breakdown between net-new-supply & existing-unit-sales of condos in Tokyo since 2000. As by far the largest city in Japan & with condos representing the predominate form of housing there, we can safely assume that this data is broadly representative of the trends across much of Japan. As you can see, the new-build supply of condos represented almost 5x the number of existing-condo sales in 2000. Fast-forward to 2019 and we see a drastic shift, with the ratio of existing vs. new at 1.2 : 1.

The forces driving this change are numerous, though the leading causes include affordability issues, shifting cultural norms & a rapidly aging housing stock:

Building upon the above & interestingly in the opposite direction of Japan’s downward trending population numbers, total household formations in Japan are, in fact, continuing to rise (for the time being). The primary underlying driver for this being the increasing number of Japanese ultimately living alone, with a growing percentage of whom actually embracing the concept of “ohitorisama”, or a “party of one”.

Source: Mitsui Fudosan - nationwide housing stock

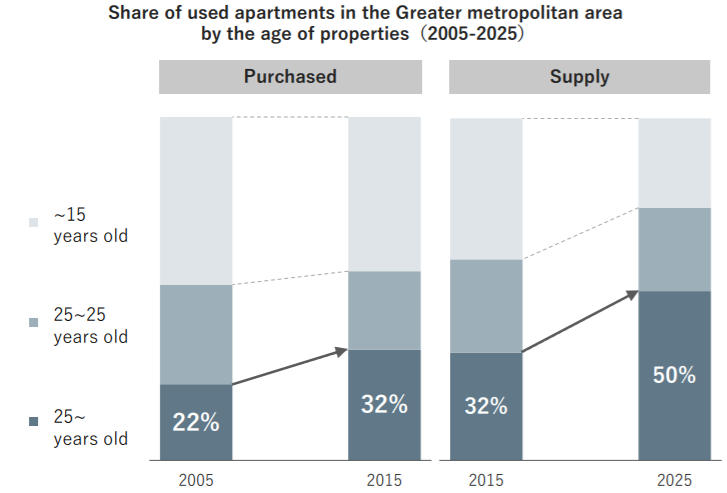

JBI note: on a related note, we came across an interesting projection regarding the housing stock in Japan…Nomura Research Institute estimates that the number of abandoned homes in Japan will reach 21.7M by 2033, or ~1/3 of all homes in the country. We’ll touch on this company in greater detail in the competitor section, but Katitas is a very sophisticated, sizable & market-leading real estate group exclusively playing in the vacant home space. A graphic from one of their recent investor presentations provides further evidence of the shifting attitudes among Japanese towards pre-owned homes:

So, just to briefly recap, we have a growing number of net-new household formations with an increasing preference for pre-owned homes, that is driven by generally structural market & cultural realities, in a market where ~50% of all homes will be >25 years old by 2025 & where the supply of new-builds has & continues to dramatically fall. I’d say that’s a pretty exciting set-up for a company building a reimagined online buying experience for renovated used homes that is primarily targeting the digital-first, younger generations who are just now beginning to enter their prime home buying years…

To tie things back to tsukuruba & to drill into the company’s immediate & medium-term TAM, we see that management guides to a ¥1.6Tn ($15.3Bn) used & renovated home market in the greater Tokyo metro area alone today, with that expanding to ¥8Tn ($76Bn) when looking nationwide by 2025.

Taken a step further, just the renovated used home market in Tokyo proper today likely stands at about ¥600Bn ($5.7Bn), growing to an anticipated ¥800Bn ($7.6Bn) by 2025.

Let’s not forget, of course, that there are several other major population centers in Japan that tsukuruba will certainly expand to over time:

Greater Osaka - 19M

Greater Nagoya - 9.5M

Greater Kitakyushu - 5.5M

Greater Shizuoka - 3M

Upon digesting all of the above, one thing becomes clear…there is a very powerful tailwind - supported by the Japanese Government - behind the enormous, growing, still relatively nascent & increasingly preferred used home resale market in Japan.

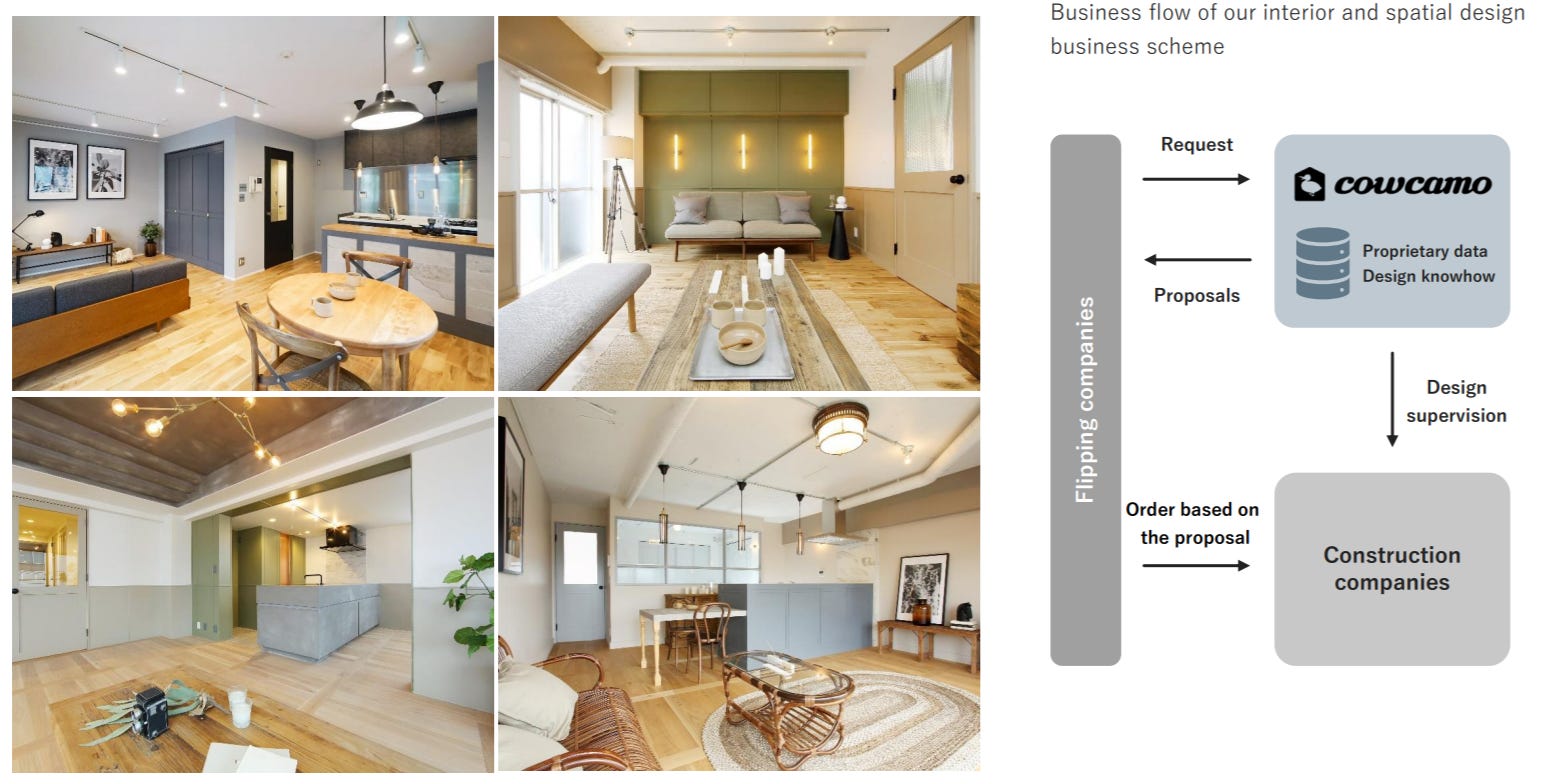

cowcamo: Reinventing, Personalizing & Digitizing The Home Buying Experience

To be clear, the cowcamo of today is not perfectly comparable to Opendoor. Rather, the product is likely more akin to Redfin’s traditional home brokerage marketplace, to where the company actively facilitates transactions between buyers & sellers, though specifically for newly renovated used properties in urban centers. cowcamo sits in the middle of this exchange, acting as a broker, an interior design / renovation consultant & a data-driven, user-friendly property guide.

“Redesigning” The Demand Side

Firstly, it is important to note that cowcamo has some serious traction among end-consumers. For FY2019 (July 2020 end), cowcamo saw an 86% YoY growth in the number of registered users, rising to 190k. This number jumped to >200k as of October 12th.

Registered MAUs are similarly growing quite rapidly at 72% YoY.

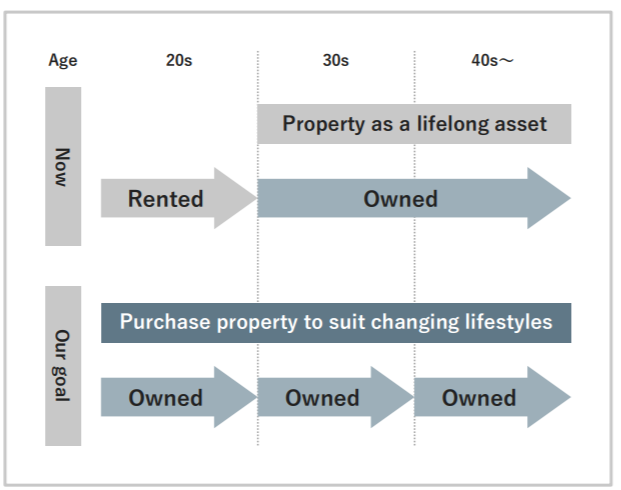

Like its U.S. peer Redfin - whose mission is to “redefine real estate in the consumer’s favor” - tsukuruba is focused on doing the same in Japan. Unlike Redfin, however, tsukuruba has the added challenge of further accelerating the (fortunately) already improving consumer perception of buying renovated used properties. Over the coming decades, if Japanese home buyers begin to even faintly resemble their global developed market peers - with existing home sales rising to, say, >50% of total home sales - tsukuruba is very well positioned to have a defining impact in that evolution and, importantly, in how renovated used properties are priced (i.e. higher) & the frequency with which they are purchased (i.e. more often).

JBI note: To provide some additional color around the above, remember that existing homes in Japan have historically been demolished once the owner vacates the property. As a result, for any existing home sales that do occur, they are often sold for very low prices - the alternative is demolition. What tsukuruba is excitingly attempting to do is infuse modern design, personality & structural durability into renovated homes / condos, leaning heavily on its internal culture of architectural creativity & home-lifestyle innovation. While only partly viable today, the long-term end-goal is for buyers to be able to customize a growing percentage of their overall used home renovation plans.

In doing so, the theory goes, buyers will begin to see renovated used homes as highly attractive, affordable alternatives to the typical “out-of-the-box” new-build “clones”. Taken one degree further…as a manifestation of their unique, individual self-perceptions & perhaps even representing a welcomed “escape”, if you will, from the conforming social pressures often experienced outside the home in Japan. Should even a portion of this envisioned reality come to fruition, there will almost certainly be a meaningful jump in the willingness to buy - as well as in the subsequent prices to be paid - for renovated used homes, benefiting not only tsukuruba, but the entire home buying ecosystem in Japan.

To elaborate on this last point, just as is the case in the U.S., Japanese home buyers may for the first time for many increasingly not only have the desire, but the confidence, to own several different homes throughout their lives as their lifestyles change, knowing that there exists a growing, vibrant resale market to support their “home investment”. It will take a long while to potentially get to this point in Japan, but along the way, tsukuruba will likely benefit from a gradually rising average sale price for renovated used homes, coupled with an upwardly trending buying frequency.

To pause for a second & provide some visual evidence of tsukuruba’s design work, check out their below projects for MoneyTree’s offices (which is btw a really interesting, foreigner founded Japanese fintech company now expanding into Australia) & its own co-working space in Takayama…pretty cool looking, right? Especially compared to the average Japanese office…

While we’re at it, let’s compare some of cowcamo’s currently listed renovated condos vs. the typical condos you’ll find around Tokyo (top are from cowcamo’s main page & bottom are sourced off generic condo listing sites). As you’ll see, there is an added elegance (in our view at least!) to the overall aesthetics, lighting, room design & furnishings.

The natural next question is presumably how the search & buying experience currently looks & feels on cowcamo. Unfortunately, we’ll leave that to readers to explore on their own, but management does provide a basic overview below:

While the primary user experience is intended to be on mobile, you can take a peek at how the company presents select featured properties on its desktop site. In short, you’ll find yourself scrolling through a walking-tour of the house, guided by the words of both a cowcamo agent & the current owners. At the conclusion, there is a floorplan alongside an estimated mortgage + other relevant pricing details, which you can flex via a provided “calculator”. All in all, a pretty unique digital experience for the Japanese market today & one in which the company intends to further improve upon by incorporating virtual reality & other incremental product features over time.

Taking a closer look at the workings behind cowcamo’s end-to-end digital buying experience, it is not a stretch of the imagination to see that management is already laying the foundations for what could ultimately become a fully integrated verticalized home buying transaction platform:

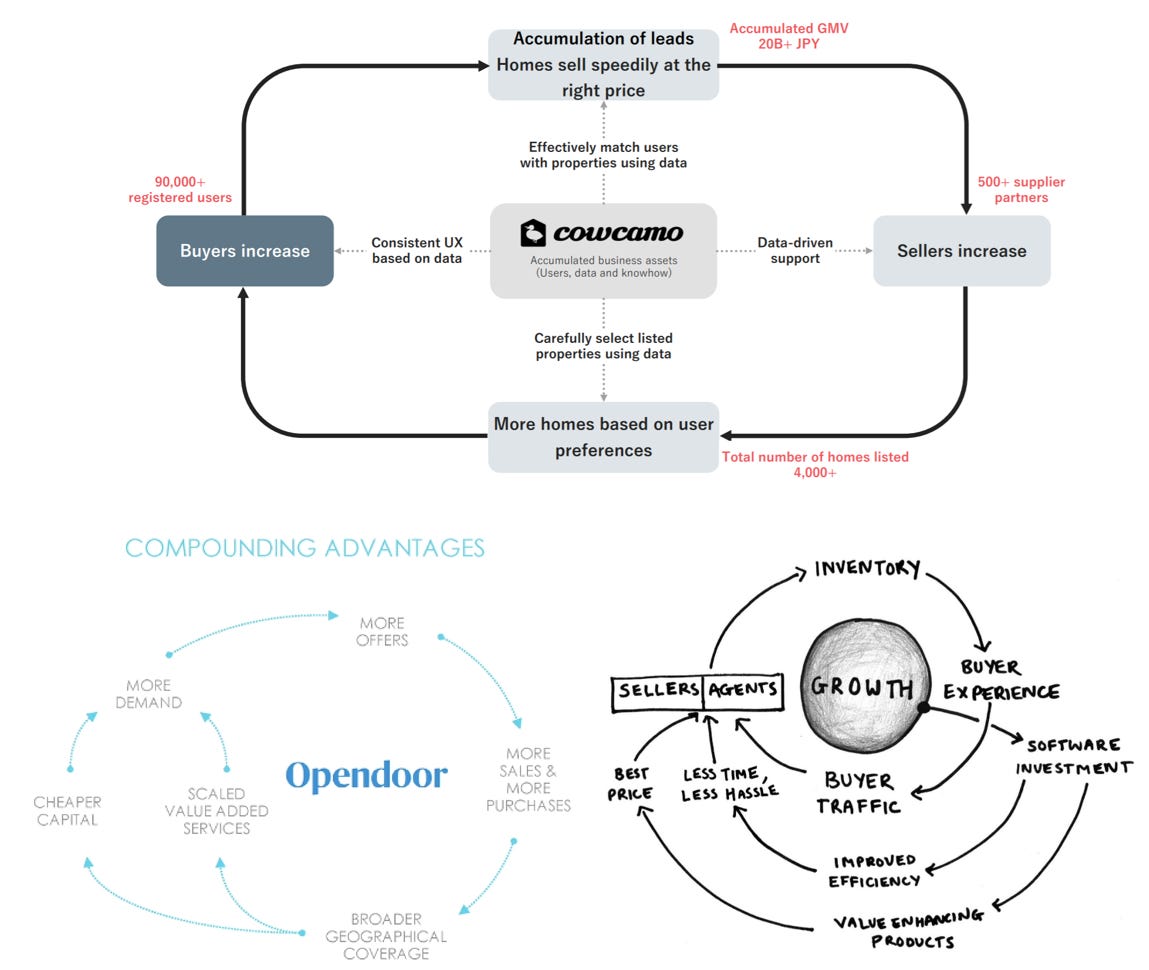

Given their growing wealth of property, user, design & transaction data, tsukuruba will have an increasing ability to continually optimize pricing, property inventory mix, target buyer profiles, renovation & design specifics & much more over time. As we have seen with the likes of Opendoor & Carvana, leveraging such comprehensive data sets is usually most powerful in markets where purchase frequency is low, “decision consequences” are high & the overall transaction tends to be more complex within a market with limited liquidity. With that in mind, we can take a peek at Opendoor to get a sense of how granular the data capture & analysis can get & the subsequent value that can be surfaced from proper use of it as well:

To segue into the next section, we can see that tsukuruba management is fortunately well aware of the power of its growing data asset in relation to & in combination with the rest of its business:

Further Investing In & Curating The Supply Side

As noted in the above graphic, the tsukuruba team has cultivated relationships with >850 supplier partners, ranging from legitimate real estate developers to individual “home flipping” groups. Unlike typical real estate listing sites, cowcamo provides its real estate suppliers with powerful data-driven insights around how best to renovate their properties to maximize the probability & pricing of home sales. This is a powerful competitive advantage in the Japanese real estate market today given that few real estate groups have the tech know-how, let alone expansive access to relevant & timely data, to arrive at similar data-driven insights on their own…even more so when targeting the increasingly important & arguably less socially homogenous cohorts of today’s digital savvy younger home buyers.

To improve the quality & depth of its marketplace liquidity, management has explicitly stated in recent earnings presentations that they are actively seeking to strengthen the supply-side. This will entail further diversifying & growing their core “enterprise” property suppliers, though likely more important, also expanding the long-tail of individual used home suppliers. Over time, many of these latter individuals will have previously been or will hopefully become buyers on cowcamo…just as we should see with Opendoor in the U.S. as time progresses.

Putting It All Together

For most of those reading this post, the general growth “flywheel” commonly cited when discussing Opendoor or Compass, for example, should intuitively make sense when applied to cowcamo as well. Fortunately, it would appear the concept is not lost on tsukuruba’s management team:

Source: cowcamo, Opendoor, Compass

To place the above into a more timely & concrete context within cowcamo’s business today, we can see below that management has clearly identified a couple of very interesting potential go-forward paths for the company over the medium-term.

JBI note: we’ll first note that we are excited to see that management is clearly being thoughtful about the future of the business & appear to grasp some of the compelling opportunities before them today. While realizing we need additional information & insights from management to truly understand the above envisioned go-forward paths, we are nonetheless initially most intrigued by i) the franchise model; and ii) the “private label” properties, if you will.

Regarding the latter, we view this as most likely being the “Opendoor model”. However, without further information from management, it is tough to judge the extent to which tsukuruba will likely want to, and frankly may (not) even need to, pursue the more capital-intensive execution strategy being pursued by Opendoor - more on this later.

With regards to the franchising angle, our immediate reaction is to take pause. One, we simply don’t have a deep enough understanding of what the team has in mind here & two, we get a bit nervous when we attempt to imagine precisely that. While we appreciate the likely rationale & perceived attractiveness of this strategy - scalability at high incremental margins - we get anxious when thinking about i) the increased risk & subsequent second-order effects of an “inconsistent user experience” at the part(s) of the “transaction stack” most controlled by an individual franchisee; and ii) the presumed long-term reality where the “sales operation model” is powering an entirely digital buying experience. If we reach such a world - which we think will be the case over the next several decades, if not sooner - who exactly is paying you a franchise fee & what are they actually doing at that point? Now, of course, we realize that world is not today, we certainly don’t have any clear idea of what that full digital buying experience will even actually look like at that point & we also very much appreciate that just because a “fully” digital buying experience may be in the cards down the road, the timing, intricacies & full extent of that transition will certainly vary by country & culture as well.

Again, these are just our initial reactions to the basic information thus far provided; we could be misunderstanding things. We find it a bit fruitless to try & speculate too much here. Moreover, as is apparent when reading the latest earnings transcripts, management themselves are not even set on these paths at this point.

Significant Future Optionality

As astute investor Dennis Hong of ShawSpring Partners recently commented in an October 2020 interview:

“The best management teams create optionality & they’re very very thoughtful about using the resources at their disposal to chase after that optionality”

Running with this insight, there exists an exciting array of highly complementary products / services that tsukuruba can appended to cowcamo to drive incremental customer happiness and additional profitable revenue over time. Looking to the U.S. market for some initial inspiration, we’d highlight a few examples:

Block Renovation - a renovation platform that combines architect-grade design, construction labor, fixtures & materials into affordable renovation packages.

JBI note: tsukuruba is arguably already doing this in ways with its partner “flipping companies” & general contractors, though packaging it up into a more consumer-facing product, as Block has done, could both efficiently & meaningfully expand the “long-tail” supplier pool among individual sellers (the ideal ultimate seller, as noted earlier). This could be done by either i) directly promoting this renovation offering as a prudent investment leading up to an already envisioned sale, ideally on cowcamo (e.x. $5k for a particular stand-alone renovation package or $4.5k for renovations & an exclusive listing on cowcamo...something to that effect) and / or by ii) winning “mindshare” among those simply renovating to improve their current homes, but who may at some point down the line end up seeking to sell…on cowcamo (i.e. profitably sell them renovations today to establish a relationship & to plant the seed for a future sale on cowcamo “tomorrow”…basically a call option of sorts on a CAC-advantaged future revenue stream).

Welcome Homes - operates as an online residential real estate platform that aims to turn home buyers into home builders by creating a more seamless, price transparent & fully customizable home buying process.

JBI note: as broadly touched on earlier, we see the Welcome Homes approach as a likely & straight-forward “product extension” for cowcamo

Additionally, in thinking about one of the more talked about topics today among “platform” tech companies, tsukuruba could embed lucrative financial products directly into the cowcamo user experience. Examples would include mortgage lending, home insurance, furniture purchase financing and / or installment payments for additional renovations.

JBI note: we won’t dive into this topic, but similar to Opendoor, you can see how cowcamo could one day become the “digital home” for all things related to one’s home (i.e. buying / selling homes, mortgage financing, furniture shopping, related financial products, ongoing renovations, home repairs, etc.).

Moving to another topic ripe with optionality, there are three active partnerships that cowcamo has today worth mentioning. The first two are with Marui & Star Mica.

JBI note: a version 1.0 JBI drafted a post on Star Mica awhile back that we’d encourage readers to check out - a pretty interesting, unique, very Japan-specific real estate investment model).

With regards to Marui, tsukuruba issued ~$7M in 0.5% interest, 5-year convertible bonds with a conversion price of ¥1,200 to Mauri in July 2020. Mauri is a $4Bn market cap company operating in the retailing & e-commerce, credit card & broader fintech spaces. The group has >7M active credit cardholders - 95% of which are <40 years old - which they intend to leverage in building out a broader array of “lifestyle” related offerings. Examples of such offerings today include rent guarantees & renter’s insurance. Interestingly, Marui management anticipates the rent guarantee business becoming a >$200M internal business by 2025 on $8.5Bn worth of rent payments, achieved in large part via partnerships with third-party home & condo builders primarily catering to Gen Z & Millennials (latest Marui investor presentation).

Presumably, the basis for the tie-up with tsukuruba, and cowcamo more specifically, is with a similar end-goal in mind: to provide their young credit card customer base with a relevant, digital-first home buying experience, as these customers advance into their prime earnings & home buying years.

With regards to Star Mica, the partnership is more straight-forward. In short, Star Mica acquires condos, renovates them & subsequently sells them. They are a well-oiled machine today & naturally view cowcamo as an attractive marketplace on which to not only list their condo inventory, but whose audience they can very specifically cater to by tapping into cowcamo’s growing data asset as well:

Through this alliance, Star Mica and tsukuruba will jointly create a new sales system that allows buyers to select renovation design patterns from “cowcamo,” one of Japan’s largest renovation property media. tsukuruba will utilize the market data of cowcamo’s [now >200,000] registered users to develop design patterns based on consumer preferences. This will enable purchasers of (pre-renovated) Star Mica properties to select their favorite renovation designs from multiple patterns.”

Lastly, as it is a quite new, though very exciting, partnership, we have few details about it; however, tsukuruba recently formed yet another business alliance with the $2.2Bn market cap, highly popular consumer personal finance & SMB focused accounting + ERP SaaS provider, Money Forward, in September 2020. Notably, Money Forward has ~10.5M individual users as of July 2020.

At a high-level, it appears cowcamo will work with Money Forward to not only directly connect their two platforms, but to also specifically develop a real estate asset focused visualization & tracking application for Money Forward’s existing "Money Forward ME" product. More generally, this free app automatically aggregates & tracks one’s financial accounts such as bank accounts, credit cards, brokerage & FX accounts, pensions, etc. (think: Intuit’s Mint product). Suffice to say, this partnership should greatly expand cowcamo’s “top-of-funnel” user acquisition efforts, at the very least.

Competition Exists, But tsukuruba Stands Apart

As noted earlier, tsukuruba is laser-focused today on redefining & improving the renovated used home buying experience for consumers. Such a mission & offering is a powerful point of differentiation in a competitive domestic field where very few take a genuine first-principles approach to developing strategies & business practices that intimately resonate with consumers in today’s fast-changing, increasingly digital world.

JBI note: as we have touched on previously, we are of the opinion that the Millennial & Gen Z generations are to be an even more profound relative change agent in Japan than elsewhere around the globe. While we are not suggesting there will be a total deconstruction of existing Japanese thought, cultural beliefs & societal behavior, we do feel these younger generations - who are fast entering their prime earnings, child-bearing & defining cultural + political years - are carrying with them a relatively increased risk-appetite, a stronger desire to exude their personal styles & thoughts & a more global, social & inclusive view of the world around them. While generally subtle, slow to emerge & particularly difficult to identify in a given company’s one-off financial statements, this demographic “change of guard” will increasingly reward those companies who are willing and able to lean heavily into these dynamic, shifting market realities. The same can be said for other global markets of course, but we are particularly bullish on innovative Japanese software / technology companies given the very large, idiosyncratic domestic market opportunity (i.e. tough for foreign groups to compete & succeed), coupled with the highly favorable competitive dynamics when considering the almost universally slow-moving, consensus-seeking & risk-averse set of incumbents across just about every industry. Some may point to government regulations as an impediment to this “disruption”, but upon closer examination, you will be excited to see a relatively recent Japanese Government that is very active in promoting technological progress & breaking down barriers preventing such.

With that said, there are arguably two primary competitors today for tsukuruba. Neither, however, has any offering that is closely comparable to cowcamo at the moment.

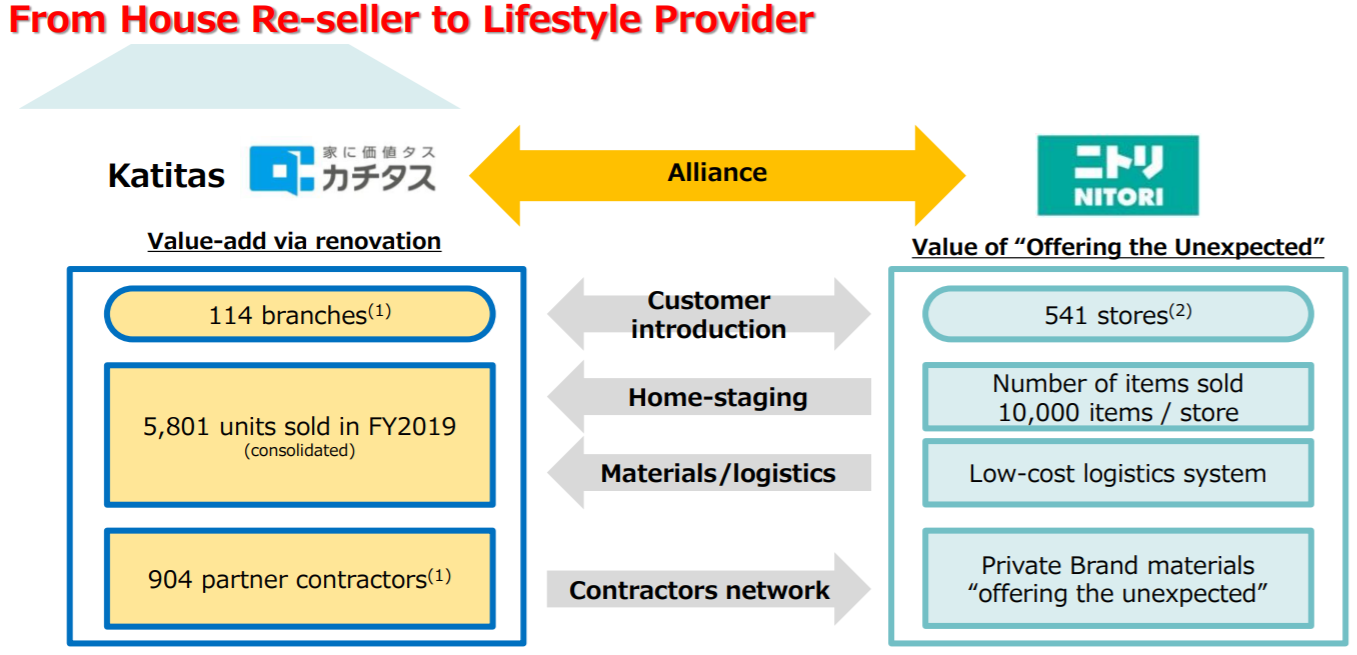

Of the two, Katitas has the greater financial resources & the real estate operating know-how to best step into cowcamo’s turf, as the company is deeply experienced in the home renovation space. Publicly listed in December 2017 after several years of ownership by Japan based private equity firm Advantage Partners, Katitas has since grown into a ~$850M revenue business with a market cap of ~$2.2Bn.

Unlike cowcamo, Katitas outright purchases generally vacant homes in regional cities across Japan that are commonly referred to as the “fourth option”. Once acquired, they fully renovate the homes & leverage an extensive salesforce + satellite office network of 114 stores to sell its on-balance sheet inventory to individual buyers.

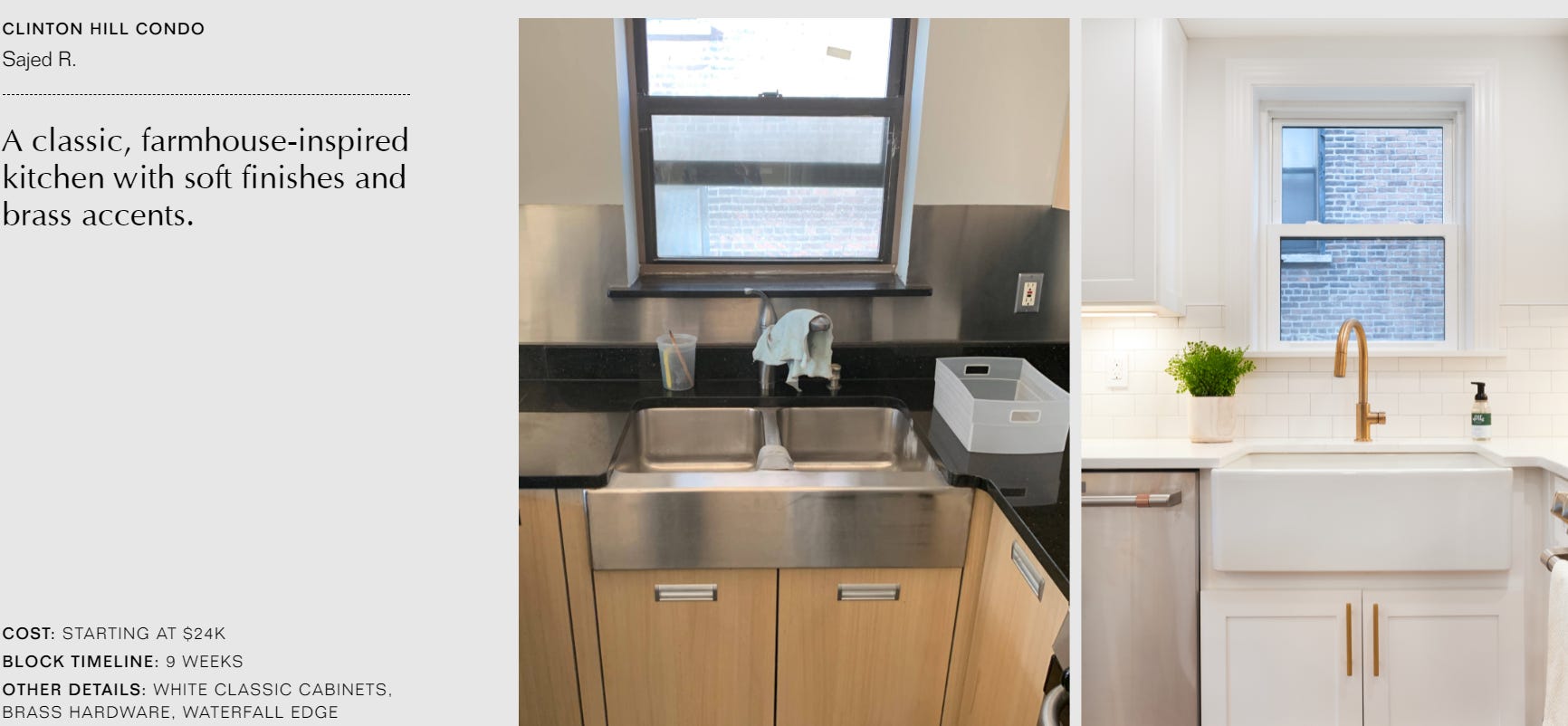

While Katitas does provide a valuable service & a quality product (see above before & after pictures), the company is confronted with the now standard innovator’s dilemma in attempting to compete head-on with cowcamo. To do so, they would need to meaningfully “restructure” their SG&A, PP&E, internal culture, target customer + asset profile, shareholder base & much more. While such a transition is certainly plausible, it would not be quick nor easy, particularly in light of Katitas’ up-until-now limited tech DNA.

JBI note: we are actually big fans of Katitas more generally. They benefit from the same macro tailwinds of that of tsukuruba & have an almost insurmountable scale, data & reputational advantage over their competitors across their focus geographies. We would not be entirely surprised to - perhaps - see a partnership form between cowcamo & Katitas at some point. With complementary i) geographic focuses (urban vs. more rural); ii) business models (digital-only vs. “brick & mortar”); & iii) asset intensity (i.e. asset-lite vs. asset-heavy), combining the two in some fashion could, in fact, see a whole that is worth multiples more than the parts.

It is also interesting to note that $23Bn market cap furniture & interior products retailer Nitori Holdings owns 34% of Katitas. One could easily see the value-add in linking cowcamo’s platform to the extensive product catalog of Nitori to allow for in-app purchases / rentals of furniture & the like to complement a buyer’s search & ultimate purchase of a newly renovated used home / condo.

As for its other closest competitor, Lifull operates a real estate listing site alongside a relatively mixed bag of other seeming “side bets”:

Its core property listing site is the largest in Japan & is most comparable to Zillow in the U.S., Rightmove in the U.K. & REA Group in Australia. End-users can browse >4M properties by location, type, proximity to train stations, etc. Lifull charges a monthly membership fee of ¥15,000 to real estate companies / brokers to list their properties in addition to a per submitted inquiry fee and a % of monthly rent / total property sale amount.

As the largest real estate listing site in Japan, Lifull clearly has the demand-side attention & the supply side listing inventory from which to launch into an iBuying effort - again, a very similar set-up & potential iBuying playbook to that of Zillow in the U.S.. However, it appears that Lifull, at least for the time being, is more focused on expanding its core real estate listing assets outside of Japan & in also growing its real estate investment product(s).

JBI note: So, all in all, is it possible for Katitas, Lifull & perhaps some other company we’ve not addressed to come at cowcamo head-on at some point? Absolutely. Though we do not see any looming threats at the moment (let us know if we missed one!). We’d also add that the Japanese market is likely big enough today, not to mention over time, to support the existence of a few other “cowcamos”.

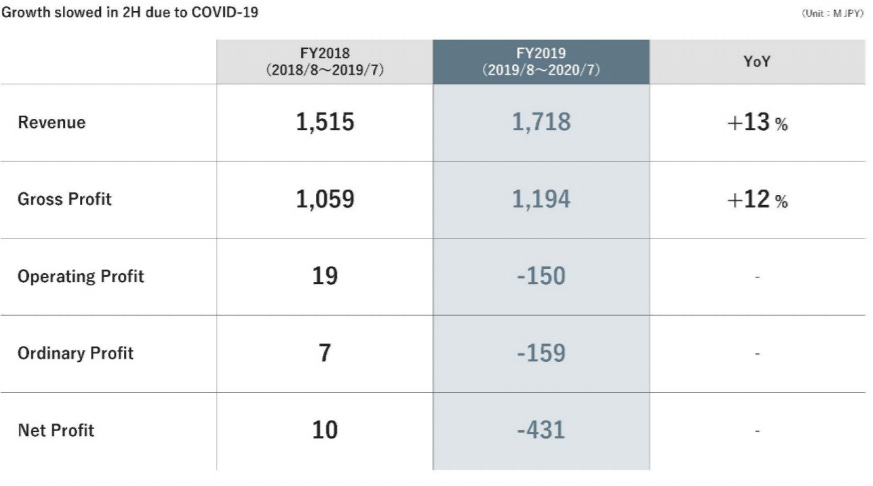

Profitable Growth & Scaling GMV at cowcamo

For their recently completed FY19 in July 2020, tsukuruba’s financials were meaningfully impacted by COVID-19. Even so, they were still able to turn in growth of 13% & 5% for the overall & cowcamo-specific businesses, respectively. Notably, cowcamo represents 78% of total company revenue, with a segment specific gross margin of 80% vs. an overall company gross margin of 69%. cowcamo was also able to clock in a 21% operating profit margin in FY2019, down from 27% the year prior.

The below graphics provide a more granular breakdown of cowcamo’s revenue, gross profit & ultimate growth drivers: the number of home purchase transactions & subsequent GMV. Of note, Q319 was when COVID first emerged on the global stage.

Important to highlight, on a gross profit basis, tsukuruba earned ~$240 per registered MAU in FY19, down 28% from $335 in FY18 - the culprit primarily being COVID. Also worthy of mention is the projected decline in FY20 (July 2021 end) overall company revenue, which management attributes to the exclusion of “resale transactions” moving forward in addition to a reduction in “corporate spot transactions”.

JBI note: so, admittedly, we are a bit confused with these FY20 revenue projections. First off, we are not very clear on what “corporate spot transactions” are, but believe these may relate to non-cowcamo revenues. We also assume that “resale transactions” occur when a buyer resells a home they very recently purchased via cowcamo, though we could very well be wrong. We’ll need to follow up with the company to gain further clarity on this.

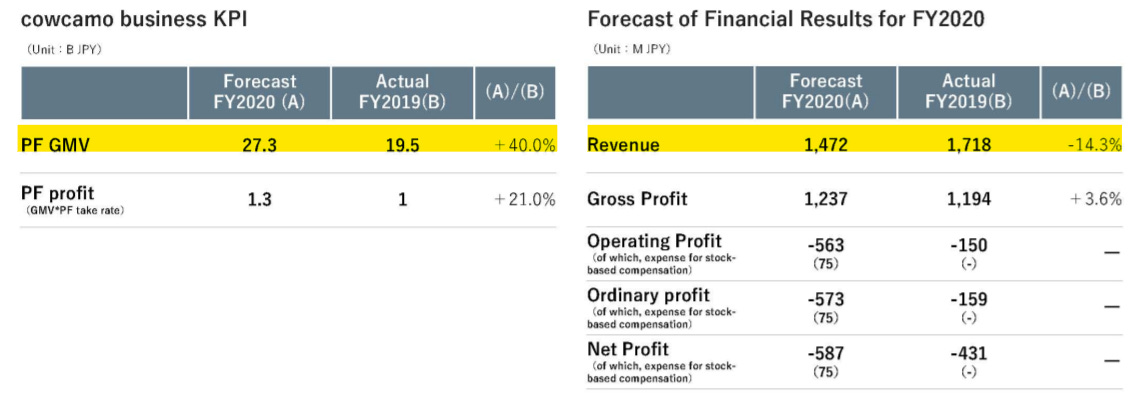

On a more positive note, management estimates a jump in cowcamo’s GMV & “platform profit” of 40% & 21%, respectively, during FY20. We won’t try to decipher things much here, but as you can see in the below graphic, it appears the company applies their “take-rate” to GMV to arrive at a “platform profit” versus what we’d initially assume: “platform revenue”. Given our current confusion, we are very eager to better understand the specifics around the entirety of the company’s various revenue models (give us a shout if anyone has a cleaner take on this!).

To playfully speculate some…with cowcamo’s GMV & platform profit both set to meaningfully rise over the coming fiscal year, yet still have an overall decline in company-wide revenue, our (likely erroneous) gut reaction is that management is effectively streamlining the business in some fashion to increasingly focus on cowcamo - as they should in our view. As a result of this, overall company revenue will understandably take a hit, thereby potentially bottoming the stock - given the relatively “ugly optics” of the FY20 financial results - just when the business is doubling-down on its “crown jewel”. In other words, an ideal time to begin building a position in tsukuruba, should you believe in the upside opportunity with cowcamo.

That said, we still don’t grasp how cowcamo had ¥1.339Bn in revenue in FY19, will grow GMV by 40% in FY20, yet have overall company revenue up a mere 10% in FY20 relative to cowcamo’s FY19 revenue alone. We’re talking ourselves in circles at this point, so that’s all for now!

JBI’s Closing Thoughts

Similar once again to Opendoor & Redfin, the long-term bet with tsukuruba is on the arguably inevitable, powerful & massive consumer behavior shift to a more digitalized, transparent, personalized & enjoyable home buying experience. Without question, cowcamo has a long ways to go to even reach where Opendoor is today in terms of scale alone. However, like with Opendoor, we see an array of upside optionality with cowcamo over time. To highlight this upside, we’ll quote Packy McCormick in his great post on Opendoor:

Opendoor will add services beyond the home sale transaction. It has announced plans for moving, but I wouldn’t be surprised if it started offering ongoing home repairs and maintenance, painting, lawn care, cleaning, and anything else related to the home that does one or more of three things:

Lets Opendoor collect proprietary data to feed into the pricing model

Keeps Opendoor top of mind

Improves the experience of living in a home

It might also flex its capital markets muscle and unique position in the real estate value chain to create a financial asset that gives investors exposure to city indices, either by syndicating out the equity it holds on its balance sheet or by giving buyers a new form of equity-based financing.

One of the core risks with tsukuruba is management’s ability to continue to execute, adapt & importantly further grow the renovated used home buying market alongside its business.

As we often like to do, we try to bridge our understanding of the generally more advanced technology industries & strategies practiced in the U.S., China & Europe with companies & opportunities in Japan. To that end, a very timely blog post by Casey Winter, Chief Product Officer at Eventbrite, was helpful as we were thinking through the opportunity with tsukuruba. In this post, Casey shares the above chart, which neatly summarizes key aspects of the various types of digital “marketplaces” in existence today.

As we feel most would agree, cowcamo falls within the “managed marketplace” segment, with the potential to move further right over time. Version One Ventures in their Marketplace Handbook defines managed marketplaces as marketplaces that “don’t just connect buyers & sellers, but take on additional parts of the value chain to offer a better experience.” Ultimately, managed marketplaces unlock net-new supply & reduce the “pain” of selling / buying by providing an added benefit / service that helps to make the transaction more seamless. Moreover, as a company moves towards the “heavily managed marketplace”, the sophistication of the value proposition offered tends to increase as well.

We’re eager to see if & when tsukuruba ever takes the leap to move cowcamo into the “vertically integrated” category & itself acquire properties, as Katitas, Opendoor, Zillow & Redfin are doing. In the back of our minds, we have a growing suspicious that they may in fact never want to, let alone need to. We’re speculating some here, but when you take a closer look at recent developments in the Japanese tech, banking & regulatory environment, you start to see the inklings of a world in which many relevant third-party organizations - those without the tech know-how, operational nimbleness and data + reputational advantages that cowcamo increasingly has - will look to partner with cowcamo. We are specifically thinking of Japanese mega & regional banks, all of whom are eager to remain relevant in a world where they face tremendous structural headwinds within their core businesses. A few examples of noteworthy developments include:

Lawmakers are looking to make it easier for banks to expand into different industries

Banks can now own >5% of startups; to open investment floodgates into fintechs

We’d give Japanese banks in particular an infinitely small chance of being able to build an internal cowcamo, so the line of thinking here is that one or more mega / regional banks potentially steps in to become tsukuruba’s de facto mortgage lender(s) / balance sheet, while becoming a shareholder in the process.

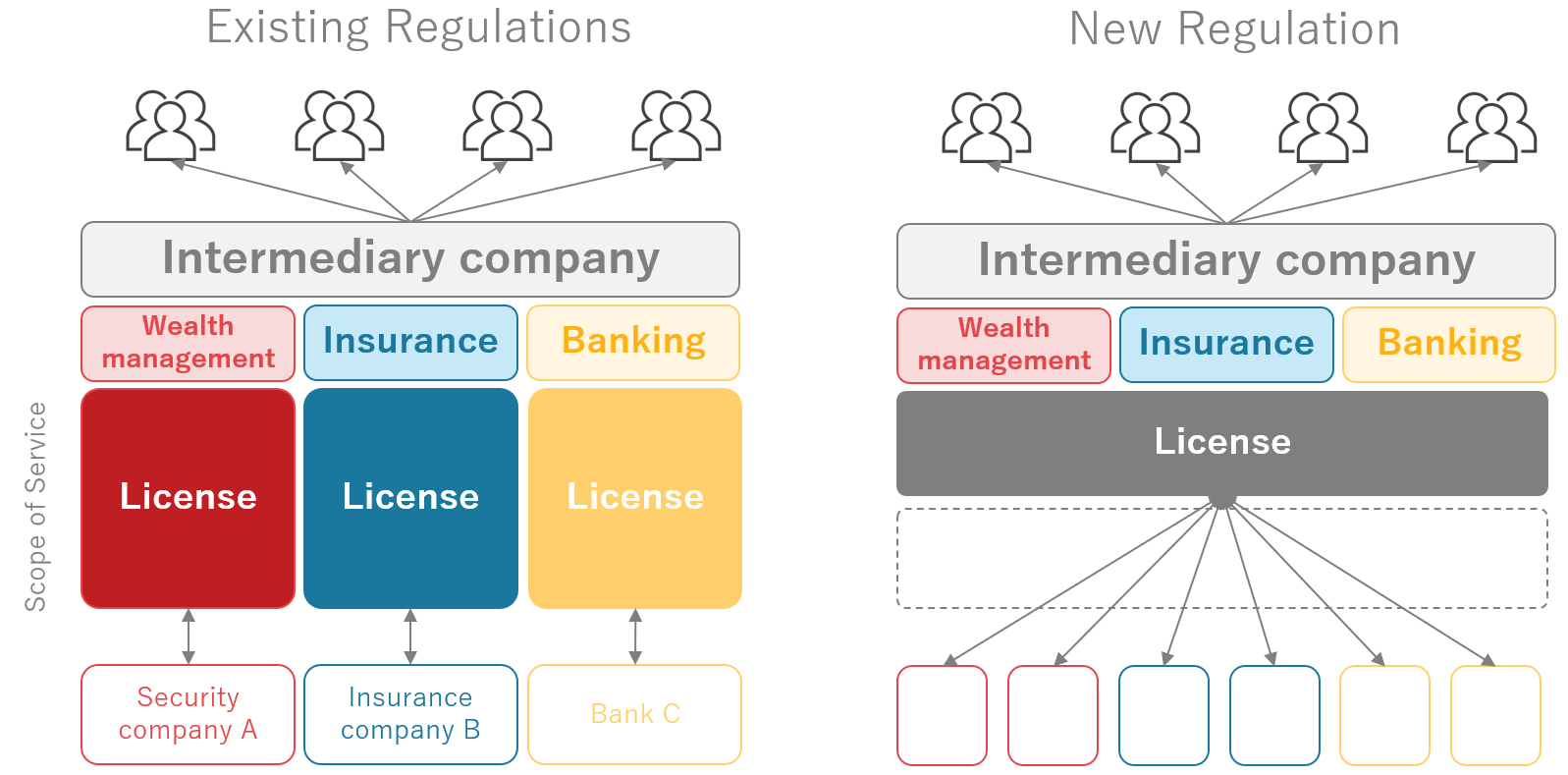

One-Stop “Financial Services Intermediary Business” License - July 2020

This post aside, the above is absolutely huge. What this regulatory change effectively allows is as follows:

If you aren’t aware, getting a license for just about anything in Japan is extremely difficult, let alone for highly regulated financial services. With the above change, companies will now be able to far more easily & aggressively push out an array of “embedded finance” products across their digital properties that have strong existing consumer adoption. This will be a boon for the API driven fintech space in Japan (i.e. Japanese equivalents of SoFi’s Galileo, Plaid, Finix & Drivewealth) & for startups + non-financial consumer-facing companies alike.

As mentioned at the start of this post, we view tsukuruba as an “early-stage VC bet in the public markets”. There is a lot that needs to play out for an investor to see VC-like returns from investing in the company today, which will, of course, take a lot of time…a time horizon that may be too long for most public investors valuing the company today. On top of that, FY20 will likely see a declining topline, which will not optically screen well among most investors.

As a result, it is tough to imagine there being much near-term investor enthusiasm about tsukuruba until we begin to see further scaling & success flowing through into reported financials. Nonetheless, when taking the coveted long-view & looking ahead to the end of the decade, we don’t think it is far-fetched to envision a world where cowcamo is seeing >10,000 home sale transactions a year with a GMV of >$4Bn (remember: the company projects a GMV of ~$260M on >600 transactions for FY20).

One last thing to highlight on the topic of management compensation…while not as aggressive as we’d like (i.e. shorter timeframe, higher targets & more options), the latest stock acquisition rights set to be issued to management in November 2020 (with a ¥1,045 exercise price, 39% above today’s price of ¥753 per share) will require a doubling of gross profit to ¥2,500M for them to be 100% exercisable.

To close…we return to Opendoor one final time. As most know, Chamath Palihapitiya’s Social Capital Hedosophia Holdings Corp. II is merging with Opendoor. Opendoor is being valued in the transaction at 1.0x 2019 revenue of ~$4.7Bn - which, mind you, is equivalent Opendoor’s effective GMV (i.e. the aggregate total sales price of all homes it sold in 2019). tskuruba, on the other hand, is today valued at just 0.29x its FY19A (July 2020) & 0.22x its FY20E (July 2021) GMV of ¥19.5Bn & ¥27.3Bn, respectively (on an EV basis). By no means a perfect apples to apples comparison, but close enough to cause one to pause & think twice…

As Chamath said of Opendoor: “These guys are my next 10x idea”. Well, we think tsukuruba could be our next 100x idea. Only time will tell!

PS do you guys have any idea of what happened with the jump in revenue from 531m (FY2017) to 1,515m (FY2018)? It is quite concerning to me because it looks like the company was trying to drive up the top line ahead of the IPO

Thanks for the article and the website guys! I’ve recently focused a lot of attention on the Japan Mothers stocks after first learning about Base, as I was an early Shopify investor and completely understand the potential there. I have in fact reached virtually identical conclusions to what you guys have written here, so it is a pleasure to find that there are people out there who hold the same view. I look forward to your upcoming articles and, again, thank you for sharing and making all this available in English!